27 February 2026 |

Academy Trusts Achieve Best Financial Performance Since 2022 but Confidence Remains Fragile

Written by Kevin Connor, Head of Academies, Bishop Fleming

Academy trusts post strongest finances since 2022 - but sector confidence remains strained

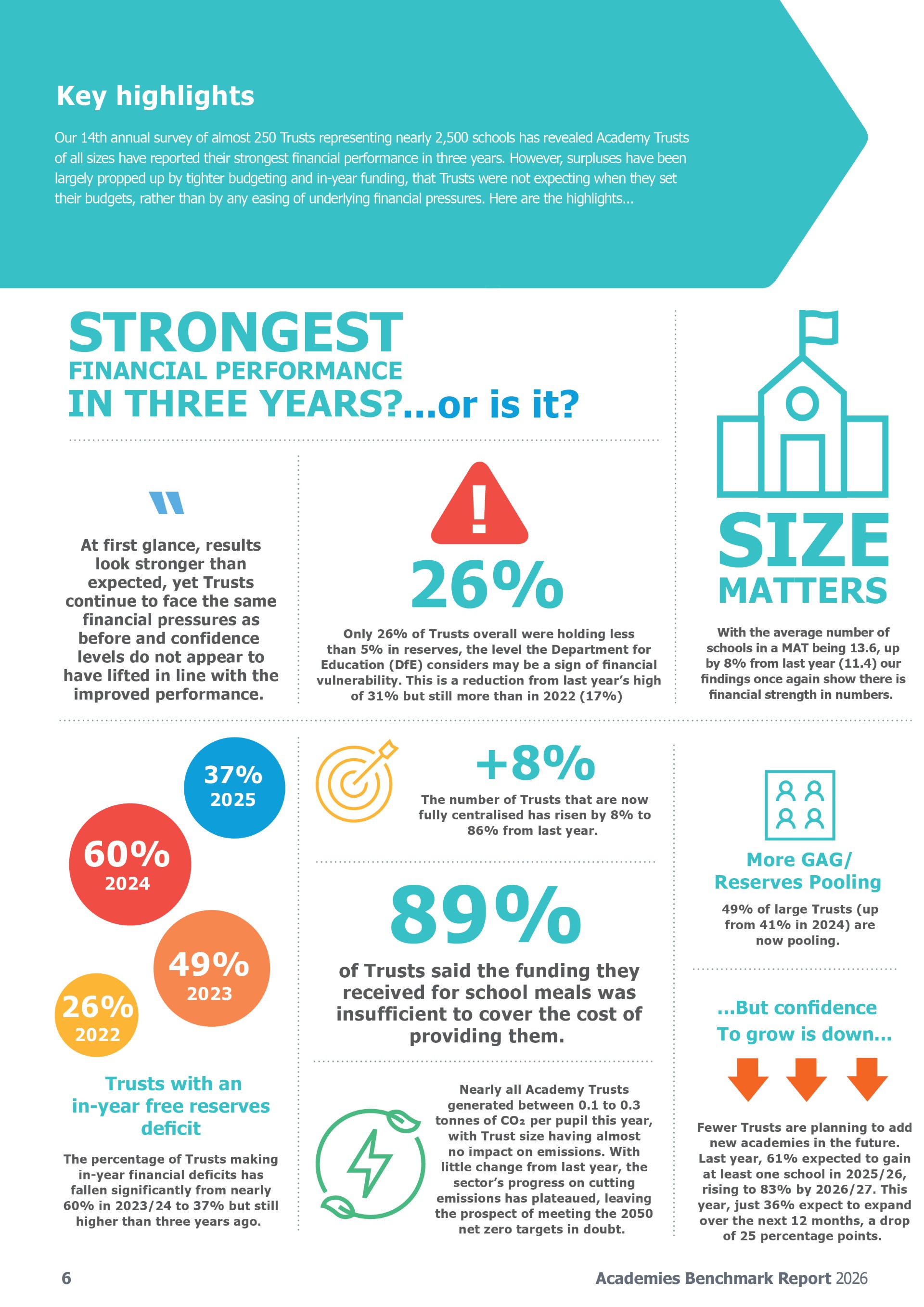

After several turbulent years for the academies sector, the latest Academies Benchmark Report offers a rare piece of positive news. Trusts recorded their strongest overall financial performance since 2022. The improvement is significant: only 37% of trusts ended 2024/25 with an in-year deficit, compared with 60% just 12 months prior. Yet this unexpected turnaround has done little to lift confidence across the sector. If anything, trusts appear more cautious than ever, with falling reserves, rising costs and stalling growth forecasts shaping the outlook for the next two years.

This year’s results reflect a sector that is performing well on paper but feeling increasingly vulnerable beneath the surface. While budgets have balanced, the conditions that enabled these improvements are fragile, and many trust leaders believe they cannot be relied upon again.

A stronger year, but dependent on short-term conditions

The financial improvement across the sector is real, but the underlying reasons matter. Trusts benefited from particularly tight budgeting and from in-year funding allocations that were not anticipated when budgets were set. This helped many finish the year in a better position than expected. But none of these factors represents long-term shifts in the financial environment, they are tactical responses to uncertainty, not signs of renewed stability.

At the same time, pressures in core cost areas have not eased. Staff expenditure is more dominant across every trust type than ever before, accounting for more than 75% of income in 2024/25. Rising salaries, additional support staff requirements and increasing employer-side costs all continue to outpace the funding available to cover them. It is therefore no surprise that 90% of trusts now identify staffing pressures as one of their biggest financial concerns.

This improved performance in the short term, paired with long-term uncertainty, sits at the heart of the sector’s fragile confidence.

Reserves point to a future decline, not a recovery

The clearest warning sign in the report is the widespread expectation that reserves will fall sharply over the next two years. Almost every category of trust is forecasting a decline. The most striking case is among secondary Single Academy Trusts (SATs), which expect reserves to drop by 43% by 2026/27. This projected fall is not a theoretical risk but a reflection of the real pressures of rising costs that cannot be absorbed without drawing on financial buffers.

Current reserves paint a mixed picture. Only 25% of trusts hold reserves below 5% of income, the Department for Education’s benchmark for potential vulnerability. But beneath that headline figure lies significant variation. Smaller trusts, in particular, saw reserves fall from 13% to 11.5% of income, while larger trusts maintained theirs at around 8%.

The gap between larger trusts and smaller ones continues to widen, signalling a structural imbalance that strategic leadership alone cannot resolve.

Scale remains a critical determinant of financial resilience

The report reinforces a familiar pattern: larger Multi Academy Trusts (MATs) continue to show far greater financial resilience than smaller organisations. This year, large MATs returned average surpluses of £1.1 million, benefiting from greater economies of scale, broader resource pools and centralised financial models that give them more flexibility.

By contrast, SATs and small MATs reported surpluses of less than £50,000 on average. These trusts operate with much tighter margins, leaving them more exposed to unexpected costs or sudden changes in pupil numbers. As costs rise, their ability to invest, improve facilities or take strategic risks diminishes.

This disparity has significant policy implications. If smaller trusts continue to operate on shrinking margins while larger trusts stabilise, the sector risks developing a two-tiered system of financial resilience. For a model built on the idea that trusts of all sizes should be able to drive school improvement, the financial gap presents a strategic challenge.

Growth slows sharply after years of expansion

Academy trusts continued to grow over the past year, and the average trust now oversees just under 14 schools, up from just over 11 in the previous year. However, the momentum of this expansion has slowed considerably.

Last year, 61% of trusts expected to add at least one school in 2025/26, and 83% anticipated further growth by 2026/27. This year, only 36% say they plan to expand in the next 12 months, a 25%-point drop.

Such a sharp decline reflects more than a shift in ambition. It suggests that trusts are increasingly reluctant to take on new schools unless they can be confident of having the financial stability, staffing capacity and long-term resources to support them. For trusts that remain small, the risk of adding schools with complex challenges may now feel too great. For larger trusts, the question is whether rapid growth would strain their ability to maintain quality and local responsiveness.

Staffing pressures eclipse all other financial concerns

Rising staff costs remain the single largest challenge facing academy trusts. Salaries, national insurance, pension contributions and the increased need for specialist support staff are combining to create a cost base that grows faster than funding. With 90% of trusts citing staffing costs as a major concern, this pressure shows no sign of easing.

Compounding the issue is the sharp rise in the number of pupils with additional needs. This trend has driven an increase in SEND-related expenditure, stretching already limited budgets and placing new responsibilities on mainstream settings. Utilities and estate repairs are also rising, ensuring that even trusts that delivered surpluses this year face difficult decisions ahead.

Without more predictable, long-term funding settlements, this pressure is likely to intensify.

Interest rates deliver a temporary boost

One area of respite came from higher interest rates, which continued to generate additional investment income for trusts. Average returns rose to £33 per pupil, increasing to £39 per pupil in large MATs. This additional income helped strengthen reserves and provided a welcome cushion during a year of tight budgets.

But this boost is temporary. As interest rates fall, trusts will need to adjust once again to a financial landscape without this supplementary support.

Progress on net zero stalls as capital pressures grow

The report also highlights limited change in trusts’ carbon emissions, which remain between 0.1 and 0.3 tonnes of CO₂ per pupil. With no further grants available through the Public Sector Decarbonisation Scheme, trusts face real barriers to investing in the estate improvements necessary to reduce emissions. For many, the upfront capital costs remain out of reach.

This lack of progress raises questions about the sector’s ability to meet the 2050 net-zero target without renewed national investment.

A sector balancing short-term strength with long-term uncertainty

Collectively, the findings reveal a sector that is managing well in difficult circumstances but does not feel confident about the future. Surpluses have improved, yet reserves are falling. Cost pressures continue to rise, while appetite for growth declines. Larger trusts remain resilient, but smaller ones face growing vulnerability.

The underlying message is clear. Without more stable, sustainable and predictable funding arrangements, the improvements of 2024/25 may prove short-lived. Trusts can deliver strong financial management, but systemic pressures require systemic solutions.

Events

The Annual Operating Theatres Show 2026

10 September 2026

The National Facilities Management in the Public Sector Show 2026

23 September 2026

The National Achieving Net Zero in the Public Sector Show and Exhibition 2026

29 September 2026

The National Special Educational Needs and Disabilities (SEND) Conference 2026

6 October 2026

Advancing Women in Leadership: Balancing Ambition, Wellbeing and Impact

7 October 2026

Courses

Effective Leadership Through Emotional Intelligence - CMI Level 7 Award

12 August 2026

5 spaces available

Directors Development Programme Accelerator

17 August 2026

10 spaces available

Senior Leadership Programme – CMI Level 7

18 August 2026

8 spaces available

Women In Leadership

15 September 2026

The Aspiring Leaders Programme

17 September 2026

4 spaces available